Do Nonprofits Get a 1099? How to Receive & Issue This Form

Updated On: 02/12/2026

In recent years, nearly half of nonprofit leaders have found it difficult to fill staff vacancies. A combination of economic volatility, talent shortages, and constrained resources prevents charitable organizations from finding and retaining full-time hires.

As organizations increasingly turn to independent contractors to fulfill their needs, nonprofit teams are filling out more Form 1099s and seeking answers to questions about the form, especially amid recent changes to the threshold for filing.

If you’re hiring independent contractors (or working as one), you’ll need to know the ins and outs of Form 1099. In this guide, we’ll cover everything you need to know, including:

Frequently Asked Questions About Form 1099 for Nonprofits

What is Form 1099?

Form 1099 reports payments made to non-employees (e.g., attorneys, consultants, contractors, freelancers, and other vendors). The IRS uses this form to ensure that recipient organizations report all their income from various sources, including contracted work, rent, royalties, and other non-employee compensation.

What Are the Different Types of Form 1099?

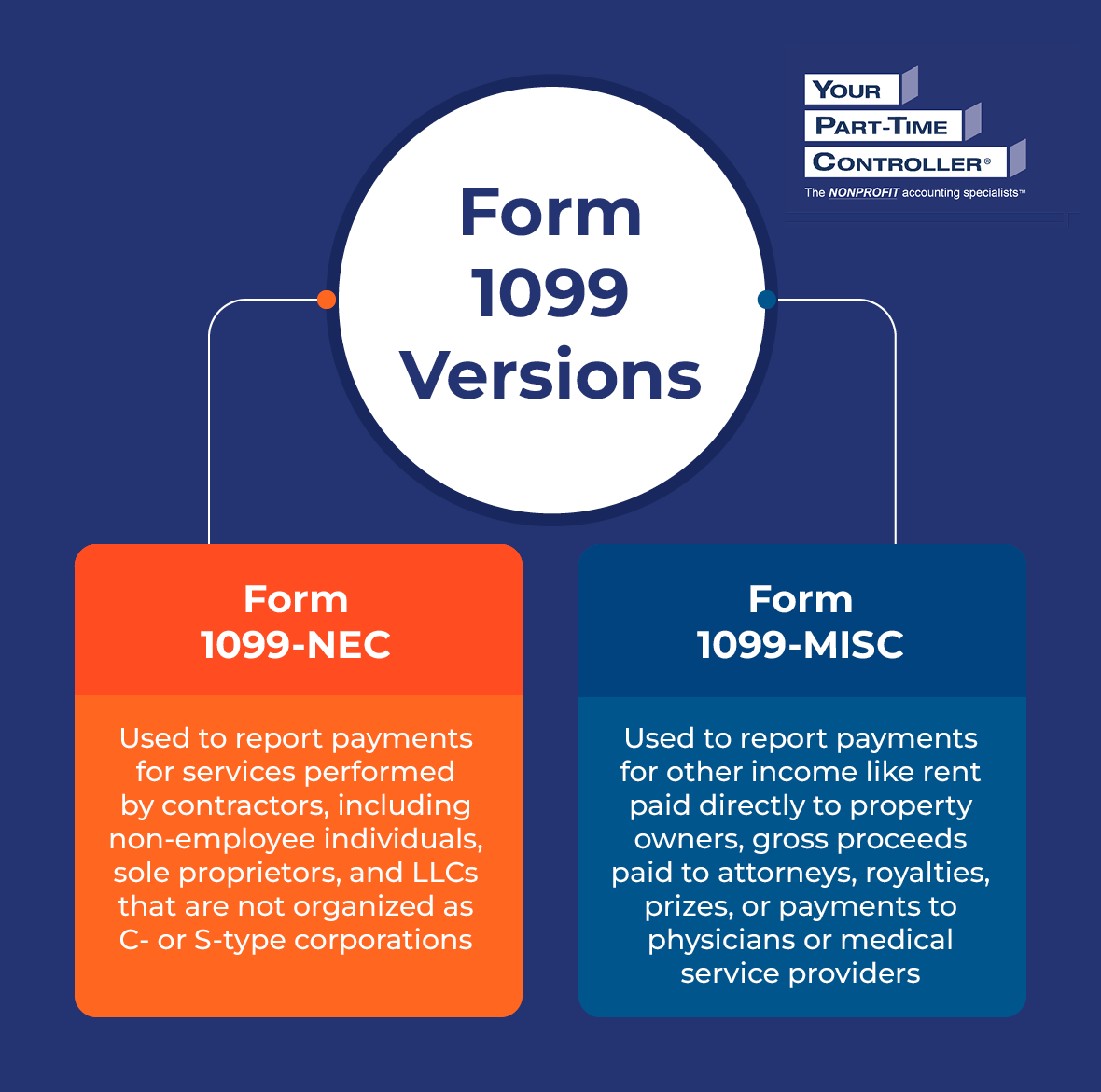

While there are many different forms in the 1099 series, this article will focus on the most common ones used by all types of nonprofits:

- Form 1099-NEC (Nonemployee Compensation): This form reports payments for services performed by contractors (non-employee individuals, sole proprietors, and LLCs that are not organized as C- or S-type corporations). Examples include fees paid to consultants and professional service providers like accountants and attorneys, as well as paid trainers, speakers, or event coordinators.

- Form 1099-MISC (Miscellaneous Information): This form reports payments for other income like rent paid directly to property owners, gross proceeds paid to attorneys (not service fees—those go on 1099-NEC), royalties, prizes, or payments to physicians or medical service providers. Rent paid to a realtor or property manager is an exception; in those instances, the agent or manager is responsible for filing Form 1099-MISC to report rent paid over to the property owner.

When Do Nonprofits Get a 1099?

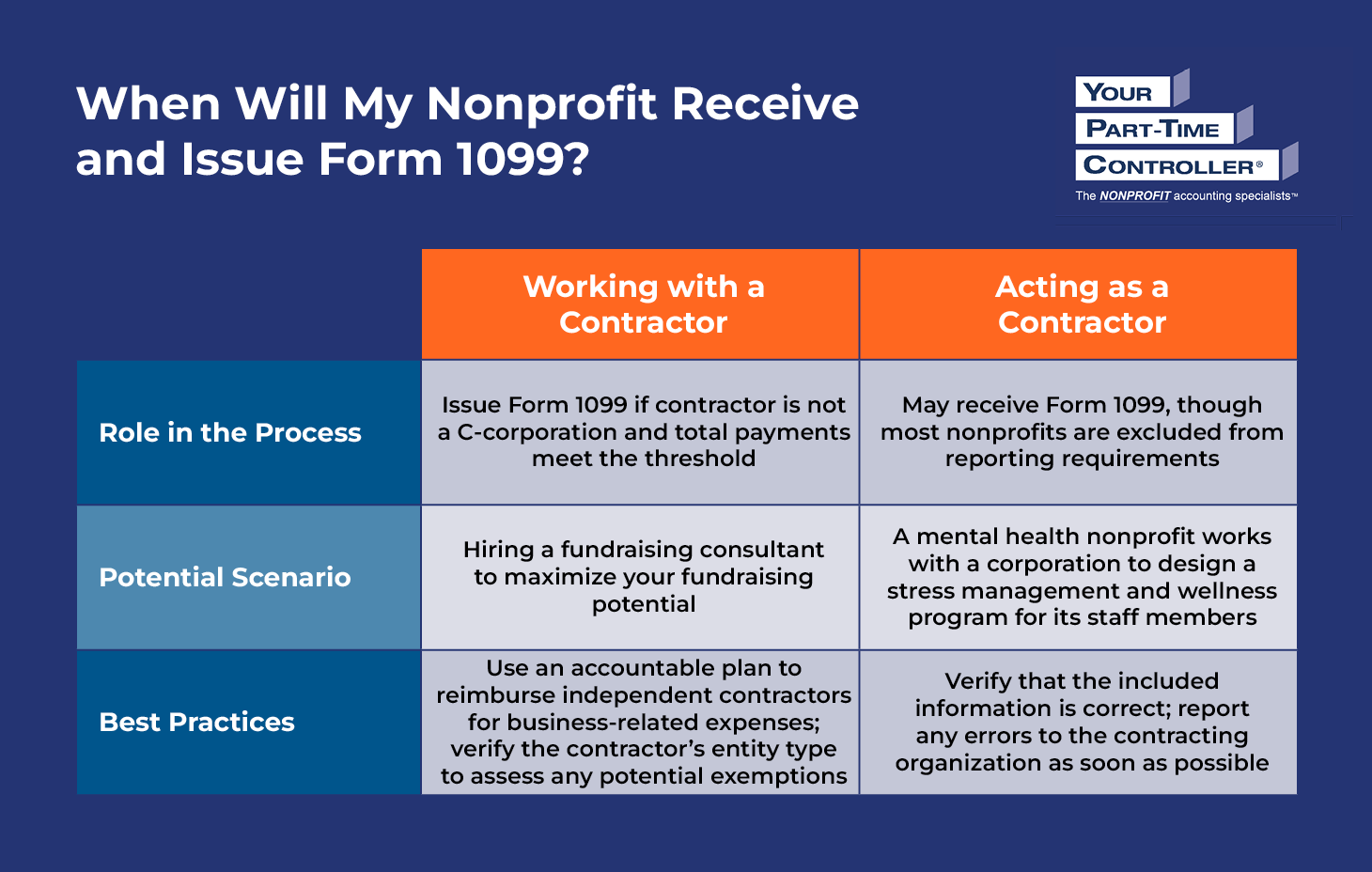

Nonprofits may earn income when they act as contractors to provide services to another organization or business. For example, a mental health nonprofit may work with a company to design a stress management and wellness program for its staff members.

Nonprofits might also rent out space or property to another organization or business. Even though this income could be taxable, the Instructions for Form 1099-MISC and Form 1099-NEC state that payments made to a tax-exempt entity are exempt from reporting. Therefore, technically, nonprofits should not receive 1099s. In practice, however, they often do. Payors issuing 1099s often do so conservatively, following a “when in doubt, send it out” approach, because it is the payee’s responsibility to determine their own tax liability.

If your nonprofit receives a 1099, you should review it to make sure the information is correct and then work with your tax preparer to determine if the reported income is taxable. Receiving Form 1099 in itself does not signal liability for the nonprofit.

When Do Nonprofits Issue a 1099?

Nonprofits issue Form 1099-NEC when they pay a contractor at least $2,000 (for years 2026 and later; previously, the threshold was $600). Common scenarios in which nonprofits issue a 1099-NEC include:

- Professional services. For example, you may hire a fundraising consultant to maximize your fundraising potential, or outsource your accounting, graphic design, and website development needs.

- Contracted program services. For example, you might hire a contractor to run a certain program, workshop, or event.

- Contracted maintenance. For example, you may hire an independent plumber, electrician, or cleaning service.

Nonprofits issue Form 1099-MISC when they pay at least $10 in royalties or at least $2,000 (for years 2026 and later; previously, the threshold was $600) in rents directly to property owners, prizes, medical payments, gross proceeds to attorneys (not fees), and certain other income payments. Common scenarios in which nonprofits issue a 1099-MISC include:

- Rent. For example, you may lease your nonprofit’s office facility directly from the owner.

- Royalties. For example, education-focused nonprofits may pay royalties to authors of their published textbooks and online courses.

- Medical payments. For example, your nonprofit may pay participants it recruits for medical research or clinical trials.

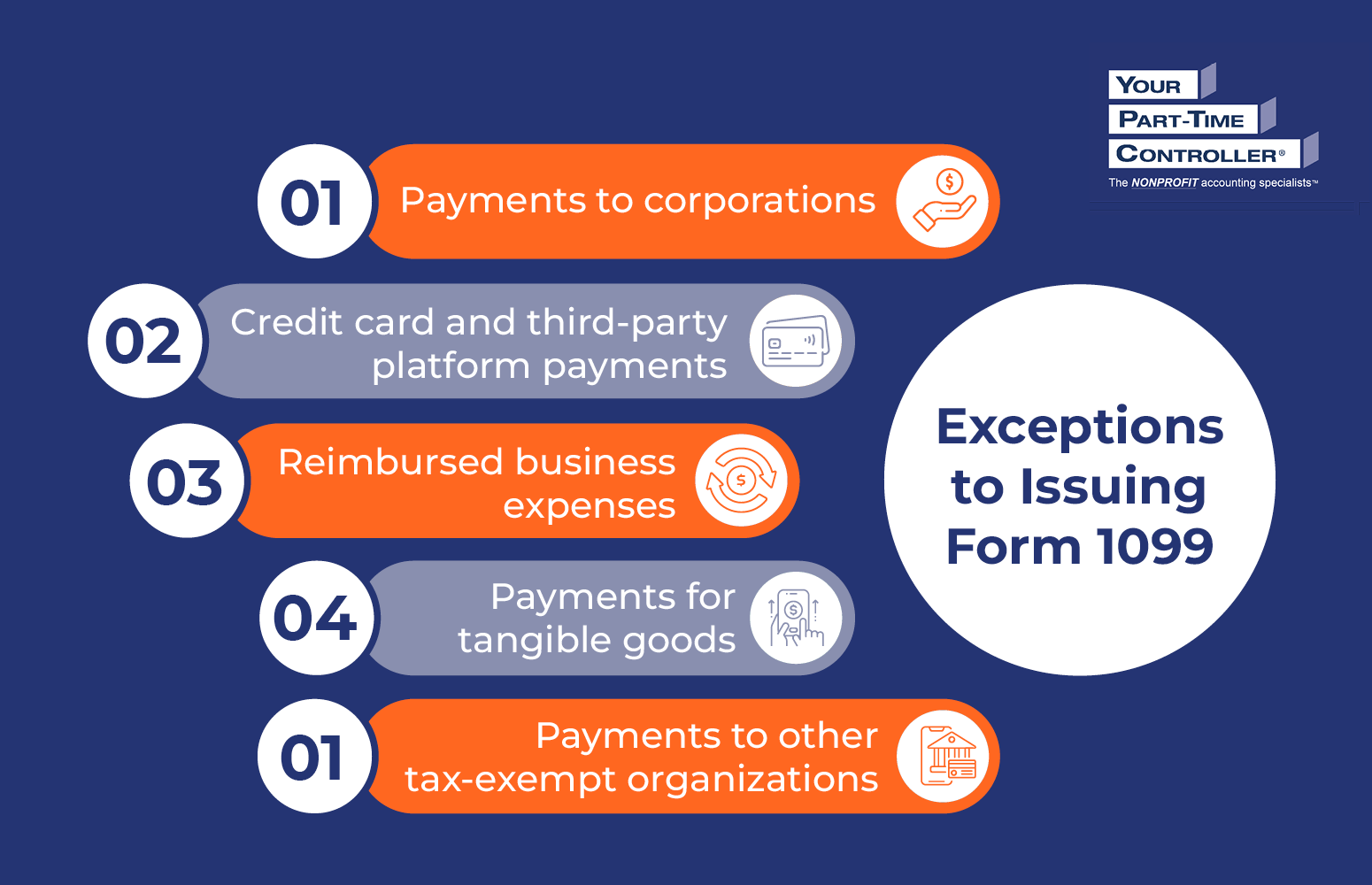

When Do Nonprofits Not Need to Issue a 1099?

There are certain situations in which your nonprofit works with an independent contractor but does not need to issue a 1099. These situations include:

- Payments to corporations. Generally, nonprofits don’t need to issue 1099s to C-Corporation or S-Corporation businesses (including LLCs treated as C- or S-corporations). Exceptions include corporations that provide legal or medical services to your organization.

- Credit card and third-party platform payments. If your nonprofit pays a contractor using a credit card, debit card, or third-party payment system, the payment entity will report those payments on Form 1099-K and issue that form to the contractor.

- Reimbursed business expenses. When you use an accountable plan to reimburse independent contractors for business-related expenses—such as travel or supplies—you don’t need to issue a 1099 because reimbursements aren’t considered income. However, to exempt these payments from taxation, they must have a clear connection to your nonprofit’s mission and associated receipts or substantiation provided in a timely manner. Additionally, the contractor must return any excess funds to your nonprofit.

- Payments for tangible goods. Since Form 1099 reports on services, you don’t need to issue a 1099 for any goods you receive. This includes merchandise, as well as freight, storage, telephone, and similar charges, unless the contractor provides goods along with their service. For example, a plumber who fixes a leak by installing a new part is completing a service, and the part installed is incidental to that service, so you would still issue them a 1099 for the entire amount you paid them.

- Payments to other tax-exempt organizations. Nonprofits typically don’t have to issue a 1099 to other tax-exempt organizations or trusts, or to a foreign, federal, or state government agency. However, you should always request a W-9 from any independent contractors, so you have their information on file and can prove exemption to the IRS. Remember to verify an organization’s tax-exempt status to ensure this exemption applies.

What Are the New Updates to the Form 1099 Requirements?

For payments made on or after January 1, 2026, the threshold for 1099-NEC and 1099-MISC reporting has increased from $600 to $2,000. This will generally decrease the number of forms small nonprofits have to file in early 2027.

What Are the Form 1099 Filing Deadlines?

Federal filing requirements mandate that organizations file Form 1099-NEC on or before January 31, meaning they must send 1099s to the appropriate recipients and file with the IRS before this date. For Form 1099-MISC, organizations must issue the form to recipients by January 31 and file the form with the IRS by February 28 for paper filings and by March 31 for electronic filings. If your nonprofit doesn’t file the form on time, IRS penalties will apply.

You may also have to file Form 1099 with the state where the recipient lives or the income was earned, especially if state withholding applies. Be sure to check with your tax advisor or your state department of revenue to confirm applicable requirements.

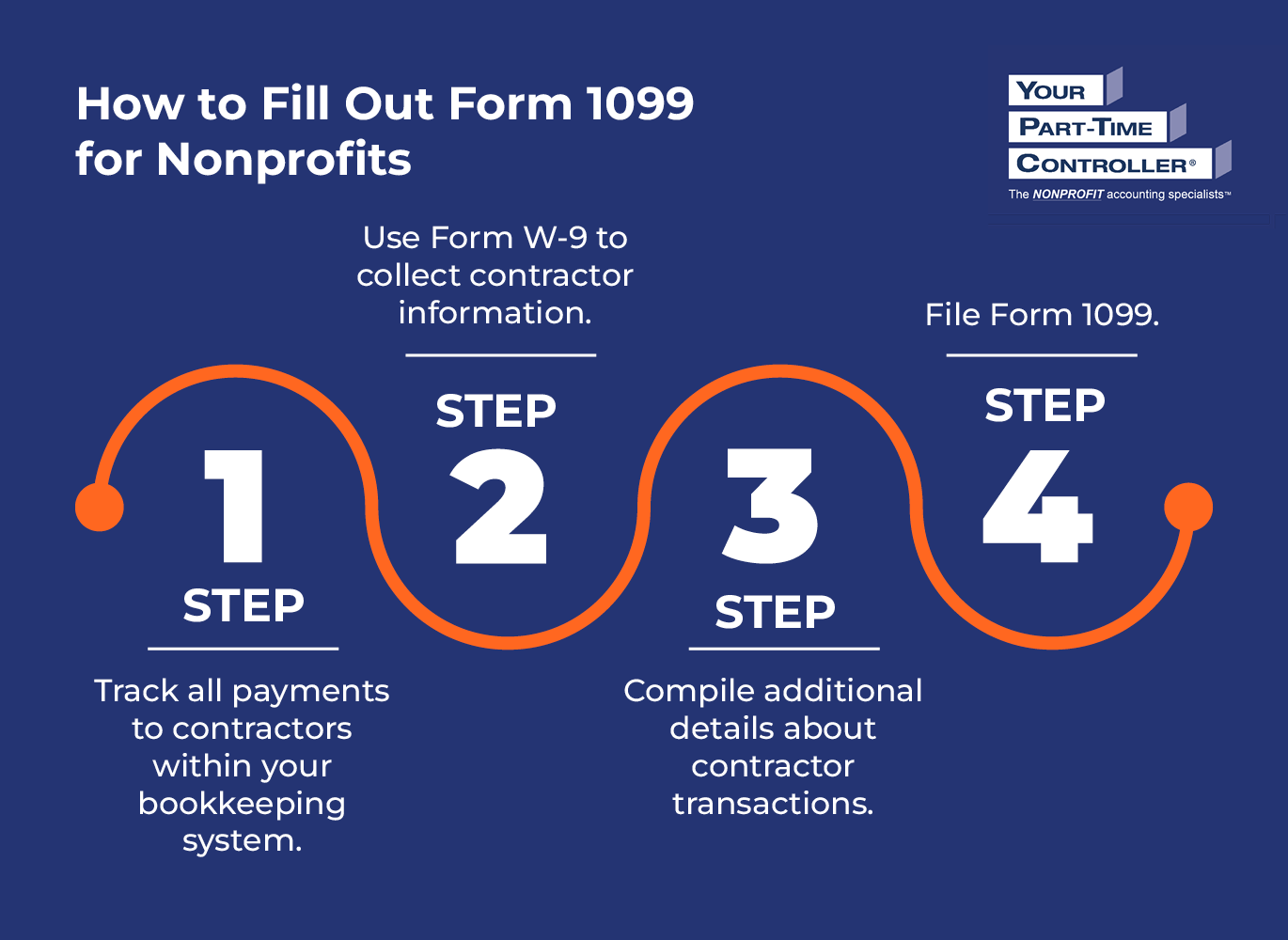

How to Fill Out Form 1099 for Nonprofits

To fill out Form 1099, you’ll start by tracking all payments to contractors within your bookkeeping system. This step creates a solid foundation for reporting by keeping relevant transaction information in one place.

Then, you’ll use IRS Form W-9 to collect contractor information. This form is also known as the “Request for Taxpayer Identification Number and Certification,” as it allows you to collect a contractor’s:

- Tax Identification Number (TIN)

- Name

- Type of entity

- Mailing address

For best results, request a W-9 form from each contractor you work with at the start of your working relationship. That way, you’ll have all the information you need to report your transactions and file Form 1099 well ahead of the deadline. If your nonprofit acted as the contractor, you may be asked to fill out Form W-9 and provide it to the contracting organization.

In addition to the information from the W-9, you’ll need the following details to complete Form 1099:

- Category of the payments made to the contractor

- Federal and state tax withholding information

- Total non-employee or miscellaneous compensation provided

You can prepare Form 1099 on your own, have your payroll company process them, or have your accounting firm process them.

Once you’ve completed Form 1099, it’s time to file. If your organization is filing a combined total of 10 or more information returns, you must e-file. You can do so via the IRIS Taxpayer Portal, which is the IRS’s free, web-based system, or you can use 1099-capable accounting software, which can be helpful if you need to file in multiple states.

Additional Nonprofit Financial Reporting Resources

If your organization is like other nonprofits, you may be hiring more independent contractors than you have in the past, and you must know how to report the income you pay them. Alternatively, you may act as a contractor, in which case you’ll need to understand when you might receive Form 1099 and what to do next. Equipped with the information in this guide, you can successfully navigate the 1099 process, ensuring you file the form properly and remain compliant with the IRS.

If you need additional help with the 1099 process or any other financial management assistance, reach out to the nonprofit financial experts at YPTC. We’ll help you strengthen your financial practices so you can focus more on your mission. Contact us today to explore our accounting, bookkeeping, and other financial management services.

To learn more about nonprofit financial reporting, check out these additional resources:

- Are You Ready for 1099 Season? Access YPTC’s Guide for 2025 Returns. Ready to file your 1099s for the tax year? Download our guide for 2025 returns.

- How to Fill Out Form W-9 for Nonprofit Orgs: FAQs + 8 Steps. Learn exactly how to fill out Form W-9, a stepping stone to filing Form 1099.

- Demystifying the 4 Main Nonprofit Financial Statements. Explore the nonprofit financial statements required under GAAP.

Jennifer Alleva

Jennifer Alleva is the Chief Executive Officer at Your Part-Time Controller, LLC (YPTC), a leading provider of nonprofit accounting services and #65 on Accounting Today’s list of Top 100 accounting firms. Jennifer brings over three decades of expertise in accounting and leadership to her role as CEO of YPTC.

When Jennifer joined YPTC in 2003, the firm consisted of just over 10 staff members. Since then, she has helped grow YPTC into one of the fastest-growing accounting firms in the country.

Jennifer’s accomplishments include her tenure as an adjunct professor at the University of Pennsylvania Fels Institute, her frequent speaking engagements on nonprofit financial management issues, her role as the founder of the Women in Nonprofit Leadership Conference in Philadelphia, and her launch of the Mission Business Podcast in 2021, which spotlights professionals and narratives from the nonprofit sector.