Liquidity Drives Impact: Budgeting and Cash Forecasting for Nonprofits

Updated On: 07/27/2026

Posted On: April 29, 2026

It’s the week before payroll. Your bank balance looks fine—until you remember the reimbursement request still sitting in a funder’s queue, the gala invoice due tomorrow, and the restricted donations you can’t touch. If you’ve ever had that ‘wait…can we actually pay everyone?’ moment, you’re not alone.

At YPTC, we see the same pattern across nonprofits of every size and subsector: cash issues rarely show up overnight. They build when timing assumptions aren’t tracked, responsibilities aren’t clear, or the organization relies on an annual budget that doesn’t reflect how money really moves.

Read on to learn how financially strong nonprofits approach cash management, including budgeting best practices and how to get started with forecasting.

Key Takeaways

- Treat cash like a mission resource. If you can’t make payroll or pay essential vendors, programs stall.

- Separate restricted from unrestricted cash in your tracking so leadership understands what’s truly available for operations.

- Keep your budget static and use a rolling forecast to reflect reality as the year unfolds.

- Don’t ‘plug’ budget deficits with hoped-for contributions. Build revenue plans by month and by funding source.

Cash Management Essentials

Effective cash management requires continuous cash flow monitoring. Additionally, these best practices strengthen your financial management system:

- Complete monthly bank reconciliations for every account that holds funds to catch missing, duplicate, or unusual transactions and reduce fraud risk.

- Maintain clear disbursement and collection processes supported by internal controls.

- Track restricted versus unrestricted cash to understand at a glance what funds are and are not available for general operations.

- Adopt (or update) a liquidity policy with reserve targets (e.g., having three to six months of operating expenses in reserves) and define when backup resources like a line of credit may be used.

- Diversify your revenue sources to help you weather unexpected collection delays or cash shortfalls without significant disruption to your programs.

Budgeting Basics

Your operating budget is:

- Your itemized estimate of expected revenue and expenses prepared at a point in time for the upcoming fiscal year and approved before that fiscal year starts

- A roadmap for resource allocation that aligns with your mission and strategic goals

- Static, providing a benchmark for monitoring performance throughout the fiscal period

- A tool for informed, data-driven decision-making, reflecting all of your organization’s activities

The following practices will ensure your budget is useful as a planning and monitoring tool:

- Budget on the accrual (not cash) basis. Your nonprofit financial statements are accrual-based in accordance with Generally Accepted Accounting Principles (GAAP). They reflect revenues when earned and expenses when incurred. Your budget should match so that budget-to-actual comparisons are meaningful.

- Include income-statement accounts and cost allocations. Project revenue and expense line items that correspond to your financial statements and reflect your shared cost allocation methodology for completeness and consistency.

- Project both restricted and unrestricted revenue. Budgeting only unrestricted funds hides the pipeline of restricted funds fueling essential projects and activities and creates confusing variances throughout the year.

- Document your key assumptions. You’ll need these to help explain budget-to-actual variances later.

Building Your Budget: Keep it Simple

You only have so much time and resources to plan and draft your budget, so think big-picture first. Get the big pieces in place and chip away at the details later. At YPTC, we call this the “marble statue approach.”

To keep it simple, begin with your major inflows and outflows. These are your main revenue categories (e.g., major contributions and grants, special event revenue, earned revenue) and expense categories (e.g., personnel costs, direct program costs, overhead costs).

Here are our top tips, based on where we see the biggest budget gaps.

Key Inflow

- Contributions and grants: Don’t increase last year’s number by a percentage and call it done. Annual totals can look reasonable and still hide a cash crunch. Create a plan by month and by funding source. Make sure your budget reflects:

- The timing of applications, awards, expenditures, and asks versus receipt of cash

- The likelihood and probability of receiving all amounts

- Whether funding is unrestricted, restricted, or conditional

- Special events: These are often front-loaded with costs. See the impact to your cash before the event by budgeting for:

- Attendance

- Ticket pricing

- Sponsorships

- Day-of-event revenues (e.g., auctions, raffles)

- Direct expenses (e.g., venue, food and beverage, entertainment)

- Earned revenue: Tuition, ticket sales, and programs like camps are seasonal. Subscriptions and sales of goods or services may be steady throughout the year. Budget for when revenue is earned (accrual basis) and plan separately for when cash is collected.

Key Outflow

Payroll is typically a nonprofit’s largest expense, and it’s also the expense you can’t ‘wait and see’ on. A detailed staffing budget should include:

- Current roster plus planned raises or bonuses

- Vacancies you expect to fill and new positions you plan to add

- Employer payroll taxes and benefits (e.g., health insurance, retirement match, workers’ compensation)

- Timing issues like months with three pay periods (common in 26-pay-period payroll cycles)

Direct program costs and overhead costs are also typically significant outflows that you’ll want to include from the start.

Next Steps

Once the budget is approved, you’ll enter it into your accounting system and use it as a benchmark for performance monitoring over the period. You’ll also use it as the basis for creating your forecast (aka adjusted operating plan).

Forecasting: How to Get Started

While your budget is static, your forecast will be fluid. You’ll update it on a rolling basis as results come in and assumptions shift. This makes it a powerful tool for surfacing critical questions and supporting informed business decisions.

Your forecasting horizon will depend on cash pressure:

- Short-term cash forecast (usually 60–120 days but can be weekly or daily): Use this when cash is tight or timing is uncertain. It helps you confirm that you can cover payroll, payables, and near-term obligations.

- Mid-range rolling forecast (typically a rolling 12 months): Combine actual results with updated assumptions to project year-end results and cash. Use this as a tool to help you spot problems early, and take action before they become a crisis.

- Long-term forecast (3–5 years): Use this one for strategic trajectory planning (growth, program expansion, sustainability). Keep it high-level.

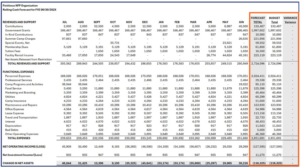

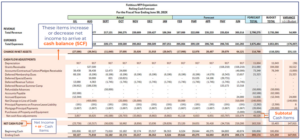

Let’s look at how to build a 12-month rolling cash forecast. You’ll do this at the beginning of your fiscal year. Here’s what you’ll need:

- Most recent set of audited financial statements

- Beginning cash balance, which should agree to the ending cash balance in your audited financial statements

- Approved annual budget, spread by month

- Assumptions schedules for key forecast elements, if applicable (i.e., detailed assumptions you documented when building your budget, such as for major contributions or payroll)

Step One: Set Up

Start with the budget as your base—spread by month, and add two columns at the right: forecast total (at set-up, this will be the same as your budget total) and variance (forecast versus budget).

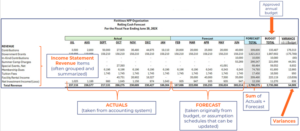

Step Two: Update

As the year progresses, you’ll update the columns of the months that have passed with the actual amounts of revenue and expenses from your accounting system and any other known or anticipated information. The amounts for months still to come with be your forecast amounts; while these were equal to your budgeted amounts to begin with, you will now adjust them as assumptions and circumstances change throughout the period.

Importantly, don’t just plug the remaining months’ amounts to meet the budget. Apply realistic, real-time assumptions and factor in seasonality and trends that have come to light since you created the budget.

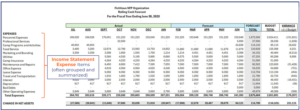

Step Three: Add Reconciling Items

Next, add a new section for cash adjustments that reconcile accrual results to cash by including balance-sheet drivers and other cash items. Forecasts that stop at the income statement miss the point. Change in net assets does not equal cash in the bank.

Reconciling items will include, for example:

- Depreciation

- Receivables and payables

- Deferred revenue

- Line-of-credit changes

- Loan principal payments

If you have comingled cash with donor-restricted funds, be sure you subtract restricted cash from your ending cash total to ensure that your forecast shows available unrestricted cash.

Now, you have a complete rolling cash forecast that you can continuously update and use to monitor trends and projected gaps. This process not only enables you to take corrective action before a cash crisis, but it also feeds into your next budget cycle, preparing you to improve your budgeting accuracy over time.

Questions Your Budget and Forecast Should Answer

Your planning tools should answer the following questions, to serve your leadership and board well:

- What will cash look like 30, 60, and 90 days from now—and at fiscal year-end?

- How much of current cash is truly available for operations?

- Which revenue or expense lines have timing risk, and what’s our plan for variability?

- What changed in our assumptions since last month, and how does that shift our cash outlook?

- Do planned hires or major purchases fit within forecasted cash capacity?

- Are we building operating reserves toward a 3-6-month target?

- Which financial indicators on our dashboard suggest we need to adjust course?

Need Support?

Budgeting and forecasting won’t eliminate uncertainty, but they will help you eliminate avoidable surprises, mitigate risk, and strengthen your financial decisions.

Watch our related on-demand webinar, Cash Is Mission: Nonprofit Budgeting and Forecasting Essentials, for a deeper dive on these topics, or check out these additional resources:

- Nonprofit Budgeting: What Your Organization Needs to Know

- Scenario Planning for Nonprofits: Building Resilience and Sustaining Impact

- Budgeting with Confidence: Creating Stability in Shifting Economies

If you want help building a budget and forecast that your staff can maintain and your board can use, YPTC can help. Contact us to get started.

Jennifer Alleva

Jennifer Alleva is the Chief Executive Officer at Your Part-Time Controller, LLC (YPTC), a leading provider of nonprofit accounting services and #65 on Accounting Today’s list of Top 100 accounting firms. Jennifer brings over three decades of expertise in accounting and leadership to her role as CEO of YPTC.

When Jennifer joined YPTC in 2003, the firm consisted of just over 10 staff members. Since then, she has helped grow YPTC into one of the fastest-growing accounting firms in the country.

Jennifer’s accomplishments include her tenure as an adjunct professor at the University of Pennsylvania Fels Institute, her frequent speaking engagements on nonprofit financial management issues, her role as the founder of the Women in Nonprofit Leadership Conference in Philadelphia, and her launch of the Mission Business Podcast in 2021, which spotlights professionals and narratives from the nonprofit sector.