Essential Church Accounting Guide: Streamline Your Finances

Updated On: 04/01/2026

Leading a church entails so much more than just dedication to your mission. Building and upholding a faith-driven community requires sufficient resources and proper financial management.

Accounting practices look different for churches than they do for for-profit organizations, and churches have a few special considerations that even other nonprofits don’t have to worry about. To help keep your finances in order and ensure proper stewardship of the funds entrusted to you, we’ll explore the basics of church accounting in this guide:

- Church Accounting FAQs

- Documents You’ll Need for Church Accounting

- Common Church Accounting Challenges

- Additional Church Accounting Best Practices

Church Accounting FAQs

What is church accounting?

Church accounting is how your church records, tracks, summarizes, and reports its financial transactions. Like other organizations, churches should follow Generally Accepted Accounting Principles (GAAP) and align their accounting policies and practices with these standards.

What is the difference between church accounting and for-profit accounting?

For-profit accounting focuses on generating a profit, whereas church accounting focuses on financial accountability and funding your mission. While for-profit organizations are accountable to shareholders for growing their earnings, churches are accountable to donors, primarily faithful members of your congregation, for responsibly using contributed funds to fuel their faith-based missions.

What is the difference between church accounting and nonprofit accounting?

Church accounting and nonprofit accounting are fairly similar when it comes to following GAAP. Churches tend to have challenges with certain aspects of financial management that we’ll discuss later on. Otherwise, the most notable difference relates to tax compliance.

While other nonprofits must file Form 990 to maintain tax-exempt status, most churches don’t have to. In addition, they’re automatically considered tax-exempt—unlike other charitable nonprofits, which typically have to apply for tax-exempt status.

Although churches are automatically tax-exempt, they may choose to apply for an IRS Determination Letter to verify their status.

What are the benefits of proper church accounting?

Proper church accounting enables:

- Stronger financial decision-making. When you carefully track, allocate, and forecast church funding, you can move from a reactive financial management approach to a proactive one. You can be more confident that the financial decisions you make will sustain your church over time.

- Better risk management. Since churches often put a lot of trust into their staff and volunteers, they don’t always implement strong internal controls, leaving their organizations vulnerable to fraud. Strengthening internal controls sets prudent guardrails and helps protect your ministry’s precious assets from fraud and theft.

- Increased transparency. The better you track and report on your finances, the more transparent you can be with your church community. Transparency fosters trust with congregants, leading to stronger relationships and more donations over time.

Documents You’ll Need for Church Accounting

Chart of Accounts

A chart of accounts lists the accounts your church uses to record transactions in its accounting system. The main categories of a chart of accounts include:

- Assets: The resources your church owns, including cash, receivables, and fixed assets like buildings and equipment

- Liabilities: Debts your organization owes, including payables, accrued expenses, mortgages, and loans

- Net Assets: Your available financial resources, found by subtracting your liabilities from your assets

- Revenue and Support: The funds your church secures through avenues like individual donations, fundraising campaigns, ministry events, and in-kind donations

- Expenses: The funds your church spends on ministries, fundraising, and administrative needs

While most charts of accounts feature these general categories, you may use different subcategories depending on your needs. For example, under Expenses, you might have a subcategory for Education that includes line items for your Sunday School curriculum, youth ministry, and adult small groups.

Budget

Your operating budget is a central financial document that helps you plan your expenses and allocate your resources for the year. It allows you to monitor your church’s financial activities and ensure you’re using funds to accomplish your mission efficiently and effectively.

To develop a strong budget for your church, make sure to:

- Start with your goals. From year to year, your priorities might shift, and your budget should reflect that. For example, if you’re looking to expand your youth programs, you’ll want to allocate more funds to the associated line items.

- Analyze historical data. Making a realistic budget requires grounding it in past performance. Identify trends in your revenue and expenses, and take these into account. For instance, if giving typically decreases in the summer, you should plan for this seasonality.

- Monitor it regularly. Every month, you should leverage budget-to-actual reporting to ensure you’re staying on track. That way, you can adjust your approach as needed to better align your activities with your budget.

Throughout the budgeting process, involve not only your finance staff members but also your ministry leaders. Their input will help you budget for their programs by more accurately projecting the associated costs.

Financial Statements

Financial statements organize your financial data so you can better interpret it and make strategic decisions. Churches use the same financial statements as nonprofits, which include:

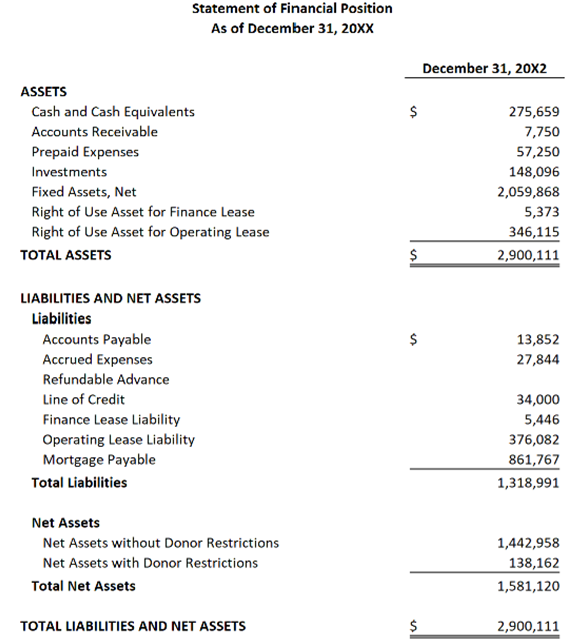

Statement of Financial Position

Known in the for-profit world as a balance sheet, a Statement of Financial Position helps you understand your church’s financial health and flexibility through its assets, liabilities, and net assets as of a point in time.

When you understand your net assets, or your currently available financial resources, you can assess your church’s financial position. Positive net assets demonstrate an excess of resources that you can reinvest in your church’s mission, whereas negative net assets mean you may need to rework your strategy to stabilize your finances.

Here’s what a Statement of Financial Position might look like:

Statement of Activities

A Statement of Activities is also called an income statement, and it allows you to analyze your revenue and expenses over a specific period. Through this statement, you can track changes in your net assets from period to period. The Statement of Activities not only informs future budgeting, but it also gives stakeholders insight into how your church allocated funding to support its mission.

Your church’s Statement of Activities might look like this:

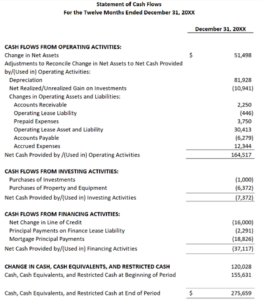

Statement of Cash Flows

With a Statement of Cash Flows, you can visualize how cash moves in and out of your church over a specific period via operating, investing, and financing activities. It shows how much cash you have available to pay expenses at the end of the period, allowing you to manage your liquidity and improve decision-making.

This is an example of a Statement of Cash Flows:

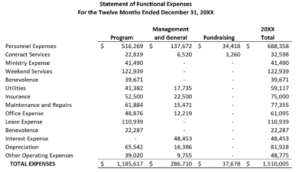

Statement of Functional Expenses

GAAP requires nonprofit organizations—including churches—to provide a functional expense analysis that breaks down expenses by nature and function. While you might do so on the face of your Statement of Activities, many nonprofits compile a separate statement to fulfill this requirement.

Churches that compile a Statement of Functional Expenses will use the following expense categories:

- Program expenses

- Supporting activities, including management and general and fundraising expenses

You’ll further break these expenses down by nature. For example, weekend services and benevolence costs are both program expenses, but you’ll separate them since they’re associated with different areas of your church. This level of detail provides transparency about your resource allocation to external stakeholders.

Here’s an example of what your Statement of Functional Expenses might look like:

Tax Forms

As we mentioned previously, most churches don’t have to file IRS Form 990, but there are some exceptions that we will discuss later in this article.

Even if you don’t have to file Form 990, you might have to complete other tax forms depending on your income and state. Familiarize yourself with the IRS page on tax information for churches and religious organizations, and investigate your state’s requirements.

Despite the differing requirements for Form 990, all churches must issue Form W-2s to employees so they can file their income taxes. You must also issue Form 1099s to non-employees who act as contractors or receive miscellaneous income from your church to ensure these individuals or organizations report all the income they receive from various sources.

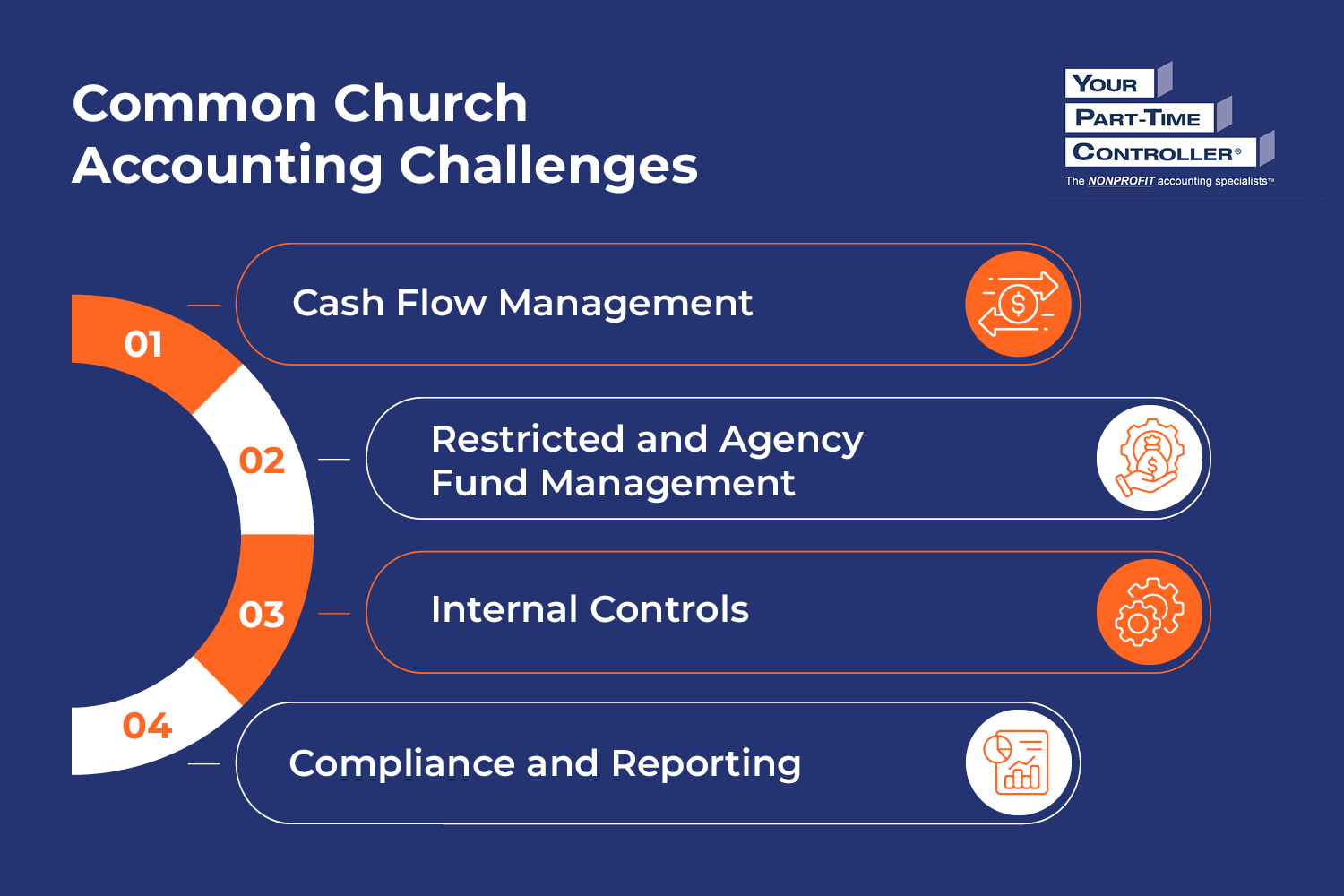

Common Church Accounting Challenges

Cash Flow Management

Churches typically rely heavily upon individual donations, making cash flow unpredictable. The following factors may prevent churches from establishing regular cash flow:

- Seasonality. Church giving and attendance often decrease in the summer, as families go on vacation. On the other hand, you may receive a significant amount of donations in December, when giving usually spikes due to year-end appeal campaigns and the Christmas season.

- Number of Sundays per month. Since Sunday services are still a primary donation collection point for many churches, the number of Sundays in the month can significantly impact cash flow. While most months have four Sundays, typically four months throughout the year have five Sundays, offering extra chances to collect support and increase cash flow.

- Lack of recurring giving adoption. Recurring giving allows you to maintain consistent cash flows, but automating these contributions requires software. Many churches still rely heavily on physical offering plates and in-person donations, which depend on attendance.

On top of these challenges, church leaders may lack the financial expertise needed to interpret financial results and recommend action items. As a result, many churches would benefit from bringing in outside nonprofit accounting experts who are familiar with church accounting and can help:

- Build cash flow forecasts and scenario plans that strengthen financial resilience.

- Budget for a surplus to establish an operating reserve that will help set the church up for success during times of uncertainty.

- Educate and train staff on financial concepts and analysis that bolster your in-house capabilities.

If you’re struggling with cash flow management, consider reaching out to a nonprofit accounting firm like YPTC for assistance.

Restricted and Agency Fund Management

Many churches confuse donor-restricted funds and agency funds—two completely different fund types that require different management strategies. Let’s explore the differences between these fund types:

Restricted Funds

Restricted funds are contributions donors give for specific purposes. Donors may contribute to broad-purpose categories, like a building fund or youth ministry, or highly specific purposes, like choir robes or camp transportation.

The level of detail in these restrictions often varies by denomination, and the more detailed they are, the more tracking effort they will require to ensure you adhere to the donors’ intent and account for them properly.

In your accounting system, you’ll record restricted funds as revenue when you receive them and as expenses when you expend them. Additionally, you’ll report on net assets with and without donor restrictions within your Statement of Financial Position.

Although donor-restricted funds are helpful for specific initiatives, churches should balance restricted funds with broader appeals to establish unrestricted cash flow that they can use for day-to-day operations.

Donors may designate their restrictions in various forms, such as:

- Solicitation materials. For example, your church may distribute a campaign brochure that tells donors what their funds given in a particular offering will support.

- Donor envelopes. When donors send physical donations, they may add a note or check a box that indicates a specific fund or purpose.

- Letters or emails. Donors may attach explicit instructions when they submit a gift.

- Memo lines on checks. Similarly, donors may write the fund or purpose they’d like their donations to go to on the memo lines of their checks.

- Digital gift notes. When giving online, donors may select a specific initiative from a dropdown menu or indicate the purpose of their donations themselves in a note.

No matter how donors submit the purpose of their funds, you must adhere to these restrictions. Failing to do so may result in donors taking legal action. To avoid this scenario, always record restricted and unrestricted funds separately, maintain detailed transaction records, and monitor expenditures in real time to ensure spending aligns with donors’ restrictions.

Agency Funds

Agency funds are amounts churches collect on behalf of another organization. Since these funds aren’t donations to your church, you should not record them as revenue. Instead, they are liabilities because your church is obligated to remit the funds to the designated third party.

For instance, agency funds might look like:

- Collections for disaster relief to be sent to an outside nonprofit

- A Mother’s Day collection for a nonprofit that serves women

- Collections for a local soup kitchen ahead of the holiday season

By classifying these funds properly, you ensure that your financial statements accurately reflect your church’s current financial position. Otherwise, your staff may think you have more resources than you actually do and plan to use those funds, when in reality, it’s money you’re holding for another organization.

Internal Controls

Churches may tend to place too much trust in their constituents, increasing their vulnerability to fraud.

In fact, according to the Association of Certified Fraud Examiners (ACFE), the median financial loss due to occupational fraud for religious, charitable, and social services organizations is $85,000 per case. Across organization types, over half of occupational fraud instances happen due to a lack of internal controls or an override of existing ones.

Internal controls protect your congregation and your church by helping mitigate the opportunity for fraud. For churches, one of the most essential internal controls is the separation of duties. Dividing responsibilities for cash handling ensures that no one person has too much control over your church’s finances, preventing them from committing fraud unnoticed.

For example, you should:

- Always have two unrelated people handle cash at all times.

- Make sure the person counting the money isn’t the one reconciling the bank statement.

While it can be challenging for smaller churches to keep financial responsibilities separate, it’s important to do so as much as possible. If you need more support, you can also involve volunteers, as long as the key controls are in place.

Compliance and Reporting

Since churches have special considerations that other nonprofit organizations don’t have to worry about, it can be challenging for them to navigate IRS rules and manage clergy-related funds appropriately. We’ll explore a few areas where churches may struggle to maintain compliance and properly report financial transactions.

Benevolence Funds

Benevolence funds provide financial assistance or aid to individuals or families. Churches often start benevolence funds to help community members in need. Since these funds are meant to benefit individual people rather than the church as a whole, there are restrictions on how you can use them.

For example, you generally can’t use the benevolence fund to help an employee or board member. This usage would violate the IRS’s strict rules to prevent private inurement in tax-exempt organizations, meaning you can’t use the organization’s net earnings to unfairly benefit anyone who has a personal and private interest in the organization’s activities. Even though most churches automatically receive tax-exempt status, private inurement rules still apply.

To prevent private inurement, you need a written benevolence fund policy with objective criteria for assessing funding requests. It’s best practice to have a benevolence committee that evaluates need-based requests for alignment with your church’s policy and approves or declines these requests accordingly.

Once your committee has accepted a request, you’ll typically submit benevolence payments directly to the vendor, such as a landlord or utility company, for the benefit of, rather than directly to, the individual you’re helping. This practice ensures the funds are disbursed for their intended purpose and helps your church remain compliant with IRS rules.

Unrelated Business Income

Sometimes, churches generate revenue from business activities, like renting out the church parking lot or running a coffee shop. The funds secured from these activities may be considered unrelated business income (UBI).

Although churches are tax-exempt and do not have to file an annual Form 990, these specific activities may be subject to unrelated business income tax (UBIT) since they’re not generated by mission-related activities. As a result, the church may have to file Form 990-T to report this income and pay appropriate taxes.

Payroll for Clergy

Licensed or ordained ministers are classified as clergy for payroll taxes. Clergy tax treatment indicates that your church treats ministers as both:

- Employees for income tax purposes. Your church should issue ministers W-2s, but federal tax withholding isn’t required.

- Self-employed for Social Security and Medicare purposes. Clergy are exempt from Federal Insurance Contributions Act (FICA) taxes and pay Self-Employment Contributions Act (SECA) tax instead, which equals both the employee and employer portions of FICA tax, totaling 15.3%. Many churches provide ministers with a taxable SECA bonus in the amount of 7.65% of their salary, equal to the employer portion of FICA tax.

Your church is responsible for determining which employees qualify for clergy payroll treatment on an individual basis. These qualifications include:

- Must be ordained, licensed, or commissioned by a recognized religious body

- Must perform ministerial duties

In addition to dual-tax status, there are a few other considerations when it comes to clergy payroll:

Discretionary Gifts

Churches often collect special offerings for the pastor called discretionary gifts. However, if money flows through the church’s accounts, it’s considered taxable compensation and must be reported on the pastor’s W-2. Gifts are only tax-free if the individual gives them directly to the pastor. Only gifts that flow through the church’s accounts should be included on the individual’s contribution statement.

Housing Allowances

Also known as parsonage exclusion, ministers can exclude a portion of their compensation from federal income tax to cover housing expenses if:

- They qualify for clergy payroll treatment.

- The housing allowance is officially designated in advance by the employee.

- The amount is approved in writing by the governing board annually.

Any requested changes to a minister’s housing allowance throughout the year must be applied prospectively, meaning your board must designate allowances in advance before implementing the change. You’ll report board-approved housing allowances on the minister’s W-2 in Box 14. The housing allowance exclusion does not apply to SECA taxes, so it is still subject to self-employment tax.

Additionally, your church should develop an accountable plan for reimbursement of other expenses, like travel and meals. This type of plan allows you to exclude these reimbursements from wages and ensures they’re not subject to withholding.

Additional Church Accounting Best Practices

Reconcile your church management system with your accounting system monthly.

Many churches use church management systems (CMS) to track congregant information, including donations. Donations are also recorded in churches’ accounting systems. The revenue reported by these two systems can differ for a few reasons, including:

- Timing differences. Sometimes, a donation is received in one month and deposited in the next. When this happens, ministry and finance records may differ until they are reconciled.

- Processing fees. Donations should be recorded on a gross gift basis in both the CMS and the accounting system. Many merchant accounts deposit donations made online via credit card net of fees (e.g., depositing $97.50 for a $100 donation less a 2.5% processing fee). The finance team must ensure the accounting system records the full gross amount ($100) as revenue, the processing fee ($2.50) as an expense, and the net amount ($97.50) as cash.

- Coding errors. Churches may raise funds for specific purposes, such as a capital campaign or new choir robes. Contributions made in response to specific-purpose appeals should be categorized as donor-restricted funds and tracked carefully to ensure they are used according to the donor’s intent and reported separately in the church’s financial statements. Donor-restriction coding errors can occur in either system—CMS or accounting. To avoid this, staff need to pay careful attention to the wording of the appeal that donors have responded to, as well as any memos, letters, emails, or other accompanying documentation.

At the end of the month, generate a report from your CMS showing all donations, pledges, and fees, and reconcile that report to your general ledger. Investigate, explain, and adjust for differences as appropriate. Be sure to maintain documentation of your monthly reconciliations, so you can easily pull it for your auditors.

Assess your accounting systems and processes for opportunities to streamline.

As you become more adept at church financial management, you may notice opportunities for improvement. Don’t be afraid to make changes to streamline your systems and processes, which will allow you to dedicate more time to your mission.

For example, instead of chasing down your staff for receipts, use an app that automates expense reimbursements. These types of applications allow your staff members to take photos of their receipts on their phones. Then, the app codes the expense and integrates directly with your accounting system.

Consider a fractional CFO or outsourced controller to help strengthen your financial management.

By now, you’ve seen that church accounting and financial management aren’t always simple. While you could rely on your existing staff or volunteers, many churches turn to fractional CFOs or outsourced controllers to take the lead.

These financial management experts can lend their expertise to your church, strengthening your practices and ensuring compliance. Plus, if you work with those who specialize in church-specific financial management—like YPTC—you can be confident that your finances are managed with best practices and focus more time on meeting your congregation’s needs.

Additional Church Financial Management Resources

Church accounting is a complicated yet necessary part of running a church. It ensures not only that you stay compliant with IRS rules but also that you understand your church’s current financial position and can make informed decisions that support your mission and financial sustainability.

If you’d like assistance keeping your church’s finances in order, contact YPTC. Our faith-based accounting specialists are happy to help with any of your financial management needs. Contact us today to get started.

For more information on church financial management, check out the following resources:

- When a Gift Comes with Strings Attached: A Practical Guide to Navigating Donor-Restricted Funds for Faith-Based Organizations. Dive deeper into properly managing donor-restricted funds for your church.

- Developing Sound Internal Controls for Your Faith-Based Organization. Learn how to create and strengthen your church’s internal controls.

- Faith-Based Nonprofit Accounting Services. Explore our accounting services specifically geared toward faith-based organizations and institutions.

Jennifer Alleva

Jennifer Alleva is the Chief Executive Officer at Your Part-Time Controller, LLC (YPTC), a leading provider of nonprofit accounting services and #65 on Accounting Today’s list of Top 100 accounting firms. Jennifer brings over three decades of expertise in accounting and leadership to her role as CEO of YPTC.

When Jennifer joined YPTC in 2003, the firm consisted of just over 10 staff members. Since then, she has helped grow YPTC into one of the fastest-growing accounting firms in the country.

Jennifer’s accomplishments include her tenure as an adjunct professor at the University of Pennsylvania Fels Institute, her frequent speaking engagements on nonprofit financial management issues, her role as the founder of the Women in Nonprofit Leadership Conference in Philadelphia, and her launch of the Mission Business Podcast in 2021, which spotlights professionals and narratives from the nonprofit sector.