GAAP for Nonprofits: How to Navigate These Core Principles

Updated On: 05/18/2026

United States Generally Accepted Accounting Principles (U.S. GAAP) are the accounting standards that guide accounting and financial reporting requirements for entities across sectors. Some standards apply to all entities and sectors, while others are industry-specific. Because nonprofits operate to further their missions rather than appeal to shareholders, there are many nuances distinguishing nonprofit accounting from for-profit accounting.

In this guide, we’ll explore those nuances and answer common questions. We’ll cover:

- GAAP for Nonprofits FAQs

- How to Implement GAAP for Nonprofits

- Common Errors in Applying GAAP for Nonprofits

GAAP for Nonprofits FAQs

What is GAAP?

United States Generally Accepted Accounting Principles (U.S. GAAP) are the standards for accounting and financial reporting by U.S. entities. GAAP includes principles on:

- Recognition – which items should appear in financial statements

- Measurement – what amounts should be reported for each element

- Presentation – what line items, subtotals, and totals should be displayed

- Disclosure – what supplemental information is needed to explain the amounts reported in the statements

Following GAAP ensures that reporting entities provide financial statements that are relevant and understandable for users, truthful and objective, comparable with the statements of other organizations following GAAP, and verifiable by auditors.

Not all charitable organizations are required to follow GAAP. However, it is considered best practice, and certain regulators, funders, lenders, and creditors may require it.

Who sets GAAP?

The Financial Accounting Standards Board (FASB) establishes financial accounting and reporting standards for public and private companies and nonprofit organizations. The FASB is an independent, private-sector, nonprofit organization established in 1973. The Securities and Exchange Commission (SEC) has designated the FASB as the accounting standard-setter for public companies. The FASB’s standards are also recognized as authoritative by state boards of accountancy and the American Institute of CPAs (AICPA). The Financial Accounting Foundation (FAF) oversees the FASB.

Do nonprofits have to follow GAAP?

While GAAP isn’t a legal requirement for most nonprofits, many choose to apply GAAP as a best practice. It may be required by:

- Certain grantors

- State regulators if revenue exceeds a certain level (varies by state)

- Charity watchdog (rating) agencies

- Accreditation agencies for higher education and healthcare organizations

Plus, following GAAP benefits your organization, which we’ll discuss in the next section.

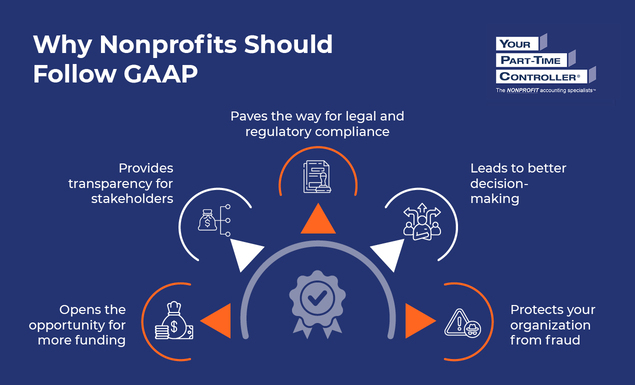

Why should nonprofits follow GAAP?

Nonprofits should follow GAAP because it:

- Opens the opportunity for more funding. Many funders, including private foundations, corporate donors, and government agencies, require conformity with GAAP or have more confidence in a nonprofit’s financial stewardship when they issue GAAP-based financial statements. Thus, following these standards can help you secure more funding for your organization. Additionally, if you need a financial statement audit to apply for a grant, you will need to follow GAAP.

- Provides transparency for stakeholders. GAAP-based financial statements help you demonstrate responsible financial management and enable stakeholders to compare your organization to others. Additionally, many charity watchdogs rely on GAAP-based data to rate nonprofits, so organizing your financial data accordingly helps them fairly evaluate your organization.

- Paves the way for legal and regulatory compliance. While GAAP itself isn’t always a legal requirement, many GAAP principles are intertwined with regulations you must follow to maintain your tax-exempt status. For example, many elements of Form 990—an IRS requirement for 501(c)3 tax-exempt organizations—align with GAAP. Also, banks typically require and review GAAP-aligned financial statements before issuing loans to assess the associated risks and ensure their own compliance with the federal agencies that regulate them.

- Leads to better decision-making. GAAP’s accrual method of accounting provides a more accurate picture of your finances. As a result, GAAP-based financial reports can help you make informed decisions that further your nonprofit’s financial stability and sustainability.

- Protects your organization from fraud. Beyond the benefits in financial reporting, following GAAP also implicitly requires having strong internal controls. By following GAAP, you will necessarily strengthen policies and processes that can help you prevent or detect potential fraud before it becomes a larger issue.

How to Implement GAAP for Nonprofits

Now that we’ve covered the value of following GAAP, let’s discuss the nuances in these standards that are unique to nonprofits—and how to put them into practice. Below, we’ve outlined ways your nonprofit can align with GAAP in its accounting approach.

Recognize revenue properly.

Your nonprofit may receive revenue from many different sources, including contributions and exchange transactions. Contribution revenue, unique to nonprofits, is accounted for differently than revenue from exchange transactions because of the differences in timing and circumstances under which nonprofits earn or become entitled to the funds.

The donor can restrict contributions for a specific time or purpose or make them conditional upon the achievement of a certain milestone or barrier. They can also make cash or in-kind contributions. GAAP’s contributions guidance (FASB Accounting Standards Codification [ASC] 958-605) provides specific requirements for recording and reporting each type of contribution your organization receives.

Revenue from exchange transactions (or contracts with customers) is accounted for similarly to revenue that for-profit organizations earn. GAAP’s contracts guidance (FASB ASC 606) specifies how to account for this type of revenue. The nuance for nonprofits: sometimes a transaction can be in part a contribution and in part an exchange transaction. In such cases, you’ll need to split up the transaction and account for the different components separately.

View our blog and related webinar on revenue recognition for a deeper dive.

Adhere to donor restrictions.

Some donors or funders impose restrictions on their contributions. Nonprofits are required to use these funds according to the donor’s intent. To ensure compliance with donor-imposed restrictions, track restricted and unrestricted funds carefully. You’ll also report them separately in your financial statements as:

- Net assets without donor restrictions. These are funds that contributors have not placed any restrictions on, so your nonprofit can use them however you see fit. Typically, individual donations made through your donation webpage, annual appeals, membership dues, and investment income fall under this category.

- Net assets with donor restrictions. On the other hand, these are funds with specific time or purpose restrictions. These restrictions might be temporary or permanent. Examples of temporarily restricted funds can include major and planned gifts, grants, and corporate sponsorships, while an endowment fund is an example of a permanent restriction, requiring the principal to be maintained in perpetuity.

By separating these funds in your accounting system, you’ll be able to comply with GAAP and maintain strong relationships with funders by ensuring proper stewardship of their contributions.

Allocate costs by function.

Under GAAP, nonprofits are required to provide an analysis of their expenses by nature and function. To fulfill this requirement, split your expenses into the following categories:

- Program expenses. Expenses that are directly related to your mission are program expenses. For example, an animal shelter buying dog food and leashes for its animal rescue program would incur a program expense.

- Supporting activities. All other expenses fall under supporting activities. This category has its own associated subcategories:

- Management and general expenses, which relate to your nonprofit’s overall operations and management.

- Fundraising expenses, which are costs incurred while soliciting contributions and grants.

Performing this type of cost allocation allows you to easily see how much of your funding goes toward your mission and how much goes to overhead, which not only helps you allocate funding in the future but also provides transparency for your donors and other stakeholders.

Prepare financial statements.

Nonprofits and for-profit organizations alike must compile a full set of financial statements to comply with GAAP. While these documents are similar, the nonprofit versions have their own unique titles and nuances:

- Statement of Financial Position. Known in the for-profit world as a balance sheet, the Statement of Financial Position reports on your assets, liabilities, and net assets. Ultimately, this statement shows your organization’s resources as of a specific date.

- Statement of Activities. The nonprofit equivalent of an income statement, the Statement of Activities shows your revenues, expenses, and change in net assets for a certain period. It reveals how well you’re managing your resources.

- Statement of Cash Flows. Similar to the for-profit statement, the nonprofit Statement of Cash Flows demonstrates how cash flows in and out of your organization. It classifies cash as coming from investing, financing, or operating activities.

Additionally, some nonprofits prepare a Statement of Functional Expenses to fulfill GAAP’s functional expense analysis requirement. It provides an extra level of transparency about how you allocate your resources and makes it easy to report your expenses on Form 990.

Common Errors in Applying GAAP for Nonprofits

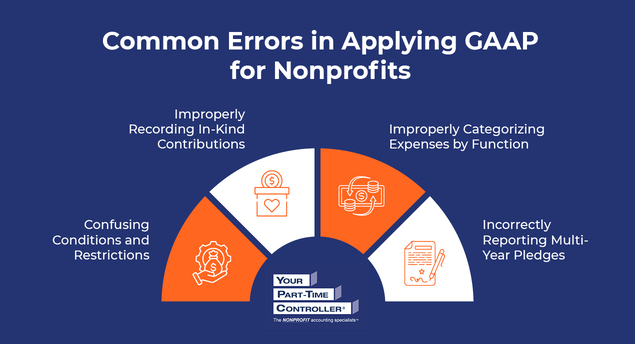

GAAP for nonprofits can be quite complex. When you understand the potential challenges you may encounter, you can navigate your accounting tasks more efficiently and know when you may need to ask a nonprofit accounting professional (like YPTC!) for help. Common errors nonprofits make when implementing GAAP include:

Confusing Conditions and Restrictions

Contribution revenue may come with donor-imposed conditions and restrictions. While both are conceptually “gifts with strings attached,” they are recorded and reported differently under GAAP:

- Conditional funds are typically grants that require you to achieve an objective and measurable barrier to be entitled to the associated funds. They must include a right of return or release, meaning that if you don’t meet the conditions, you don’t receive or cannot keep the funds. As a result, conditions affect the timing of revenue recognition. Under GAAP, nonprofits do not recognize conditional contributions until conditions are met. If the grantor provides conditional funds upfront, they should be recorded as a refundable advance (liability) on the Statement of Financial Position.

- Donor-restricted funds are contributions that have time or purpose stipulations imposed by the donor (for example, a grant awarded for a particular research study). Nonprofits are required to honor those stipulations and must carefully track these funds to ensure prudent spending and proper reporting. Donor restrictions affect how the revenue is reported, not the timing of revenue recognition. Under GAAP, nonprofits report on net assets with and without donor restrictions in the Statement of Financial Position. Additionally, the nonprofit Statement of Activities categorizes revenues and the change in net assets as with and without donor restrictions.

Pro Tip: Confusion about conditions and restrictions often occurs with grants. To ensure you identify conditions and restrictions properly, read all grant agreements carefully. Read our guide on government grant revenue recognition for further insight.

Improperly Recording In-Kind Contributions

In-kind contributions, or gifts of goods or services, allow nonprofits to access additional resources, but they can complicate financial management. Under GAAP, gifts of tangible goods (e.g., supplies, auction items) or space (e.g., facility use, advertising space) are recorded at their fair market value (FMV) as both a revenue and expense and thus have no impact on net income.

Donations of services are only recognized if they create or enhance nonfinancial assets or require specialized skills that you would otherwise have to pay for (i.e., volunteer time must meet these criteria for recognition).

In-kind contributions should be reported as a separate line item on the Statement of Activities.

Improperly Categorizing Expenses by Function

As previously mentioned, GAAP requires nonprofit entities to provide an analysis that shows the relationship between the functional and natural classifications of their expenses. This analysis makes it easy for donors and other stakeholders to see how the organization is allocating its resources.

GAAP sets out specific functional expense presentation requirements, including definitions of program services and supporting activities. While some of the rules are intuitive, some are frequent sources of error.

For example, a performing arts organization might be tempted to classify the cost of advertising ticket sales for an upcoming show as a program activity. However, the accounting standards specify that advertising costs are management and general (supporting) activities because they do not directly accomplish the organization’s mission (program), nor do they generate contributions (fundraising).

Human resource costs are another commonly misallocated expense. Since human resources staff support all other staff in the organization, many nonprofits mistakenly allocate human resource costs across all functions. However, GAAP says human resource activities are management and general, since they support the nonprofit as a whole. Budgeting and finance costs also fall in this category.

Fundraising costs include costs to solicit monetary and non-monetary contributions. This means that costs to solicit services—even those that don’t meet the criteria for recognition as revenue—should be categorized as fundraising.

For expenses that relate to more than one function (e.g., overhead costs like rent, utilities, and technology), nonprofits need to have a clearly defined cost allocation methodology. GAAP does not specify allocation methods, instead leaving them to the organization’s judgment. The chosen methods should be reasonable and consistently applied, and documenting them will help keep your organization audit-ready.

Incorrectly Reporting Multi-Year Pledges

Pledges, or promises to give, are signs of trust and sustainability for nonprofits because they represent intentions of donors to contribute funds in or into the future. Pledges have special accounting considerations that can be a source of common errors in nonprofit financial reporting.

First, nonprofits must distinguish intentions from promises to give, because intentions are not recorded, but promises are. Promises will typically be in writing with a clearly established payment schedule. Intentions, on the other hand, may just be verbal, uncertain, or unclear.

After establishing the existence of a reportable promise, nonprofits must evaluate whether the promise is conditional or unconditional. Unconditional promises to give either have no donor-imposed conditions at all or are conditional only upon the passage of time (e.g., a pledge to donate $500 next year to support the nonprofit’s overall mission) or a performance demand (e.g., a pledge to contribute $50,000 to support a specific program, paid in $10,000 installments over the next five years). Time and performance requirements are restrictions—not conditions. Remember: restrictions affect how revenue is reported, not when it is recognized.

Unconditional promises are recorded immediately as revenue and receivables at the present value of the total amount the nonprofit expects to collect in the future—even if that total spans multiple years.

In contrast, conditional promises to give are contingent on the achievement of an objective, measurable barrier (e.g., a donor promises to match a certain amount of funds that must first be raised by the organization or contribute only if the organization achieves a specific project milestone) that, if not met, releases the promisor from their obligation to give.

Like conditional grants, conditional pledges are not recorded until the conditions are met.

Additional GAAP for Nonprofits Resources

Proper implementation of GAAP sets your nonprofit up for compliance, audits, and financial sustainability. When you adhere to GAAP, you can provide financial information that is reliable and relevant for both internal and external stakeholders.

If you’d like help aligning your financial management practices with GAAP, partner with YPTC. Our nonprofit accounting professionals can help strengthen your financial operations and strategy, adhering to GAAP every step of the way. Contact us to get started.

To learn more about the best practices discussed in this guide, explore our additional resources:

- Nonprofit Accounting: What Charitable Orgs Need to Know. Dive deeper into nonprofit accounting and how to set your organization up for success.

- Demystifying the 4 Main Nonprofit Financial Statements. Learn more about each of the financial statements required under GAAP.

- Top Nonprofit Audit Preparation Guide: What You Need to Know. Explore how to properly prepare for audits and demonstrate GAAP compliance.

Jennifer Alleva

Jennifer Alleva is the Chief Executive Officer at Your Part-Time Controller, LLC (YPTC), a leading provider of nonprofit accounting services, #65 on Accounting Today’s list of Top 100 accounting firms and the #1 Best Firm to Work For by Accounting Today. Jennifer brings over three decades of expertise in accounting and leadership to her role as CEO of YPTC.

When Jennifer joined YPTC in 2003, the firm consisted of just over 10 staff members. Since then, she has helped grow YPTC into one of the fastest-growing accounting firms in the country.

Jennifer’s accomplishments include her tenure as an adjunct professor at the University of Pennsylvania Fels Institute, her frequent speaking engagements on nonprofit financial management issues, her role as the founder of the Women in Nonprofit Leadership Conference in Philadelphia, and her launch of the Mission Business Podcast in 2021, which spotlights professionals and narratives from the nonprofit sector.