Nonprofit Statement of Activities: Reviewing the Basics

Posted On: June 1, 2026

Under Generally Accepted Accounting Principles (GAAP), nonprofits must compile a full set of financial statements. These documents summarize an organization’s financial activities and health, enabling informed financial decisions and promoting transparency and accountability.

Within this set of financial statements, one you must compile is the nonprofit Statement of Activities. This guide will help you compile this document in accordance with GAAP and analyze it to better understand your financial situation:

- Nonprofit Statement of Activities FAQs

- Importance of the Nonprofit Statement of Activities

- Components of the Nonprofit Statement of Activities

- How to Analyze Your Nonprofit Statement of Activities

- Nonprofit Statement of Activities Knowledge Check (Quiz)

Nonprofit Statement of Activities FAQs

What is a nonprofit Statement of Activities?

A nonprofit Statement of Activities summarizes your organization’s revenues and expenses for a specific period of time. With this information, your nonprofit can demonstrate to internal and external stakeholders how it’s generating funds and managing resources.

Is a Statement of Activities the same as an income statement?

The Statement of Activities is the nonprofit equivalent of an income statement. However, the Statement of Activities uses different terminology and has its own nonprofit-specific considerations, such as:

- Accounting for donor-imposed restrictions

- Showing “Revenues and Support” rather than just “Revenues”

- Reporting expenses by function and nature (alternatively, the required analysis of expenses by function and nature can be reported in a separate statement or in the notes to financial statements)

- Using the term “Change in Net Assets” instead of “Net Income”

Can a nonprofit show a “profit” on its Statement of Activities?

Yes, a nonprofit can technically show a profit on its Statement of Activities, but it is not called a “profit” since nonprofits don’t operate to generate shareholder value. Instead, it’s called a surplus or positive change in net assets. Budgeting for a surplus is actually recommended to help your organization manage uncertainty or known funding gaps that could create a cash crunch and impact your ability to provide services.

How often should a nonprofit prepare a Statement of Activities?

A Statement of Activities covers a specific period—typically a fiscal year, but it can also be prepared for a month or quarter. Preparing this report monthly and comparing it to your budget for the same month can help leadership make proactive, data-driven decisions, including real-time strategic shifts that may be needed to stay on track to meet goals.

Do in-kind donations go on a Statement of Activities?

Yes, in accordance with GAAP, nonprofits include in-kind donations (non-cash gifts of goods or services) as a separate line item under Revenues and Support on the Statement of Activities. Common in-kind contributions include donations of land, buildings, and supplies. They can also include the use of facilities or utilities, advertising space, and professional services, such as pro bono legal services.

Gifts of in-kind services can only be recognized and reported in financial statements if they:

- Create or enhance nonfinancial assets

- Would typically need to be purchased if not donated

Once you determine that an in-kind contribution can be recognized, you’ll record it at fair market value as a revenue and an expense, so there is no impact on the change in net assets.

Why does my Statement of Activities show a deficit even though we have money in the bank?

Because of the impact of multi-year grants, it is not uncommon to see a negative amount reported under the change in net assets with donor restrictions column. For example, if your organization spends a significant amount of restricted grant funds in the current year that was reported as revenue in a prior year, the releases for the current year might exceed incoming contributions. Knowing the context of the restricted grant, this is to be expected.

However, a scenario that would warrant further investigation is a negative balance reported under net assets without donor restrictions. A negative balance here over multiple years could indicate financial sustainability issues.

To accurately assess the deficit appearing on your Statement of Activities, review each net assets column separately, instead of just focusing on the total.

Importance of the Nonprofit Statement of Activities

Compiling the nonprofit Statement of Activities is essential to responsible financial management because it enables your organization to:

-

- Comply with GAAP and secure institutional funding. Nonprofits must compile a Statement of Activities to fulfill the requirement of a full set of financial statements. Additionally, audited financial statements are often required for grant applications, so this statement may be necessary to access grant funding.

- File Form 990 accurately. You’ll use information from your Statement of Activities to complete Form 990. Thus, compiling a complete Statement of Activities promotes efficient and accurate Form 990 filings, helping your nonprofit maintain its tax-exempt status.

- Measure financial performance. Ultimately, the change in net assets reported on your Statement of Activities helps you understand your nonprofit’s financial performance over the period. Generally, a positive change in net assets indicates financial sustainability, while a deficit may prompt you to rework your resource allocation (more on this later).

- Improve strategic planning and budgeting. With all of your revenue sources in one place, your Statement of Activities allows leadership to easily see where money is coming from and how much is subject to donor-imposed restrictions so they can determine whether you need to further diversify income. Additionally, this document identifies your largest expenses, helping your team make data-driven decisions about funding cuts or expansions.

- Increase transparency and accountability to stakeholders. The Statement of Activities shows stakeholders how well you’re using resources to support programming and fulfill your mission. This document gives them insight into where their contributions ultimately go.

Overall, the Statement of Activities helps internal teams maintain compliance and improve decision-making while giving external stakeholders greater visibility into your organization’s funding and resource allocation.

Components of the Nonprofit Statement of Activities

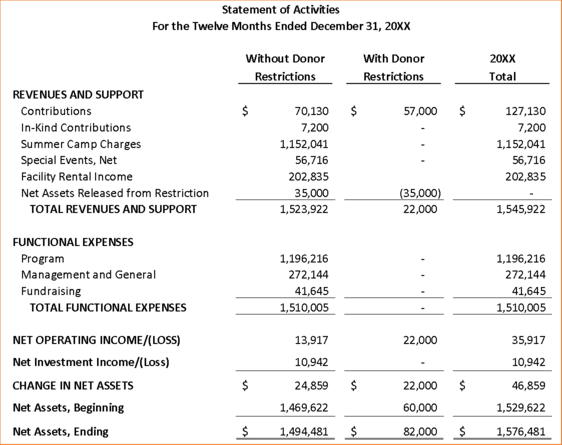

Now that you understand the importance of the nonprofit Statement of Activities, we’ll explore the statement in greater detail. Check out the following example Statement of Activities for a summer camp before diving into each section.

Revenues and Support

In this category, you’ll report resources or funds your organization receives, which may include:

- Earned revenue. Nonprofits generate earned income through exchange transactions, which occur when your organization exchanges resources of commensurate value with another party. For example, you might sell merchandise or event tickets or provide program services with associated fees, such as school tuition or clinical healthcare fees.

- Contribution revenue. Support you receive from monetary donations, pledges, and grants is considered contribution revenue when the donor or funder does not receive commensurate value in return. When you recognize contribution revenue depends on whether it has donor-imposed conditions attached, which we’ll discuss further in the next section.

- In-kind donations. According to GAAP, nonprofits must include in-kind (non-cash) contributions on a separate line in the Statement of Activities. As previously mentioned, not all in-kind contributions are eligible for recognition. For those that are, you’ll report them at their fair market value.

- Special event revenue. Many nonprofits conduct special events for fundraising purposes, such as galas and dinners. If the events are ongoing and central to operations, revenue should be reported gross. If they are peripheral or incidental, nonprofits may choose to report special event revenue net of direct costs.

- Investment income. Income from total return investing (as opposed to programmatic investing), such as investment returns generated from operating cash, should be reported net of external and direct internal investment expenses. Programmatic investment revenues are generally reported on a gross basis because they are part of a nonprofit’s ongoing and central operations.

How to Report Donor Restrictions Within Revenues and Support

Some contributed funds will have donor-imposed restrictions, meaning your organization must use them in accordance with donors’ stipulations. While these restrictions may be associated with a specific purpose, time frame, or both, all donor-restricted funds should be categorized as “With Donor Restrictions.” Only contribution revenues can be donor-restricted.

Typically, nonprofits include separate columns in the Statement of Activities for funds with and without donor restrictions, making it easier to see which funds are available for use at the nonprofit’s discretion and which are restricted by donors. If you have any net assets released from restrictions during the period, those will appear as a separate line item under Revenues and Support.

It can be easy to confuse restrictions with conditions, which are barriers that the receiving organization must overcome to receive or be entitled to funding. While restrictions affect how revenue is reported on the Statement of Activities, conditions affect when revenue is recognized. Conditional revenue should not be recognized until conditions are met.

Revenue recognition is a common source of errors and questions. For a deeper understanding, explore our nonprofit revenue recognition blog post, webinar, or government grant revenue recognition guide.

Expenses

Next on your Statement of Activities, you’ll report expenses—costs incurred to support your organization and mission. If you report expenses by functional classification, you should use the following categories:

- Program: Costs directly tied to your mission and mission-related services

- Management and general: Costs that relate to your overall operations and management, such as rent, utilities, advertising, and human resources

- Fundraising: Costs incurred in soliciting contributions and grants

Expenses are reported as decreases in net assets without donor restrictions.

Change in Net Assets

The change in net assets is the difference between your revenues and expenses for the period—similar to net income in a for-profit company. This calculation indicates whether your revenue covered your expenses for the period and how your net assets have changed as a result of your activities.

At the bottom of your Statement of Activities, you must report:

- Changes in net assets with donor restrictions

- Changes in net assets without donor restrictions

- Change in net assets in total

Most nonprofits use columns to separate these amounts. Your net asset totals on your Statement of Activities should correspond to the net asset balances on your Statement of Financial Position, so cross-reference the two statements to ensure your numbers match.

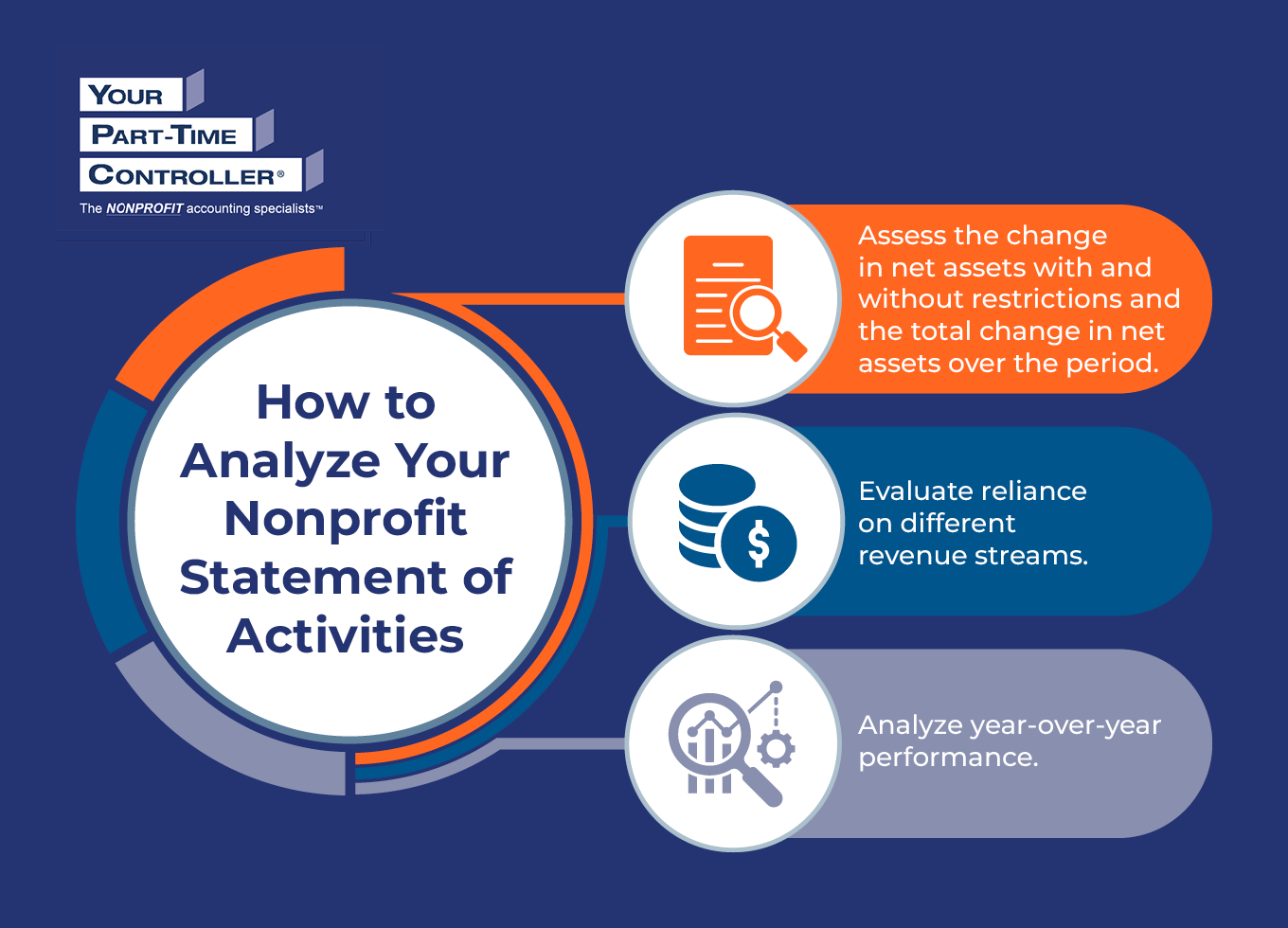

How to Analyze Your Nonprofit Statement of Activities

Once you’ve compiled your Statement of Activities, you’ll want to use the data to inform strategic planning and budgeting decisions. To get the most out of this statement, make sure to:

Assess the change in net assets with and without restrictions and the total change in net assets over the period.

These three values must be reported separately, and you should consider them separately in your analysis. Here’s what to look for:

Change in Net Assets Without Donor Restrictions

If your change in net assets without donor restrictions is positive, your organization generated more unrestricted revenue than it spent, which is typically a sign of a healthy, sustainable operating model.

On the other hand, if you have a negative change in net assets without donor restrictions, that means you spent more on your core operations than you generated and may have dipped into your savings to cover expenses. While a period or two of negative numbers in this category isn’t necessarily alarming, consistently negative amounts here could reveal a structural deficit that you need to strategize to overcome and keep your organization afloat.

Change in Net Assets With Donor Restrictions

When you have a large positive change in net assets with donor restrictions, it often means you landed a major grant, launched a capital campaign, or received some other large, restricted contribution during the period.

If you have a negative change in net assets with donor restrictions, it might mean that you spent grant funds that were recognized in a prior period. Alternatively, it might mean that you met donors’ restrictions during the period and released those funds for expenditure. In either case, a negative number in this category isn’t necessarily a bad sign and typically signals you’re actively using donor-restricted funds to fuel your mission.

Total Change in Net Assets

While a positive total change in net assets is generally preferred over a negative one, you need to dig deeper into your data to determine how you arrived at the total and what it means for your organization. You may do so by:

- Isolating non-cash and operational items. By excluding line items such as depreciation and unrealized investments from your total change in net assets calculation, you can better understand financial performance as an indicator of your core strategy’s effectiveness. In other words, you can ask yourself: “If we ignore our building aging and the stock market fluctuating, did our programs and campaigns make or lose money this year?”

- Comparing the change against your budget. Contextualize the total change in net assets against your board-approved budget for the year. For instance, if you have an accidental surplus, you may evaluate where you underspent and how you can better use those funds in the future to support your mission. In contrast, you may have allowed a deficit to intentionally draw on reserves to launch a new program, upgrade technology, or bridge a planned gap in grant funding.

- Evaluating revenue quality. Sometimes, you’ll have a positive total change in net assets that isn’t necessarily sustainable because it results from a one-time contribution or transaction. For example, a large, one-time bequest from an estate, while useful, won’t always signal overall financial sustainability and strategic effectiveness.

Evaluate reliance on different revenue streams.

To determine how reliant your organization is on specific revenue streams, calculate each revenue line item as a percentage of total revenue. Once you’ve found these totals, there are three main operational realities your organization might fall under:

- High concentration. Let’s say you receive 80% of your total revenue from one government grant. In this scenario, your organization has a relatively high revenue concentration risk. If that funder changes their priorities or cuts their budget, your nonprofit may not have enough other revenue sources to fall back on.

- Overdiversification. While, in general, the more revenue streams your organization has, the better, there are situations in which the cost of managing so many small revenue streams outweighs the financial benefits.

- Healthy mix. Ideally, you’ll have several primary, well-developed revenue streams. If there’s a downturn in any one source, the other sources will be there to provide a safety net for your organization without being overly burdensome to generate and manage.

Additionally, the types of revenue you brought in can tell you more about your organization’s operational flexibility. For example, let’s consider the characteristics of several different revenue types:

- Earned income. Typically, earned revenue is unrestricted, predictable, and proof that your community values your services. Therefore, earned income generally provides operational flexibility.

- Individual giving. Similarly, individual giving typically provides flexibility since these funds are often unrestricted. However, individual giving is susceptible to macroeconomic trends, so inflation and stock market fluctuations, for example, may affect individuals’ giving capacity.

- Government grants. While government funding can provide long-term stability (although it’s become more unstable recently), it comes with significant compliance requirements. Additionally, government grants are often restricted to specific programs and may require your organization to spend its own funds first and then wait for reimbursement from the grantor, which can strain cash flow.

- Foundation grants. If you’re launching a new program or funding a capital project, foundation grants can be beneficial. However, since foundations frequently shift their funding priorities, they could prove to be less reliable as a long-term funding strategy.

Analyze year-over-year performance.

Using comparative statements, you can identify trends and better contextualize your organization’s current financial performance. Provide explanations to your board for any year-over-year variances that exceed a predetermined threshold. For example, a slight shift in facility rental income will likely be less meaningful than a large change in program expenses.

Additionally, separate timing and permanent variances:

- Timing variances. Let’s say there was one year when you had to delay your annual gala, usually held in December, to the following March, due to a facility maintenance issue at the event venue. While this might appear to be a large year-over-year revenue drop in the year of the event delay, you know there is no cause for alarm because it is a one-time timing issue, and you have enough income from other sources to bridge the gap.

- Permanent variances. On the other hand, you may find out that a foundation you typically receive funding from has recently ended its grant program that funds your mission. In this case, the variance represents a permanent loss of revenue that you’ll need to replace.

When explaining variances to the board, don’t just restate the math. Instead, explain the variance, why it happened, and what your team will do to address it. For example, instead of saying, “Individual giving is down 20% this year compared to last year,” you might explain that this occurred because you had to cancel one of your main fundraising events due to inclement weather and will schedule an extra event early in the new year to make up for it.

Nonprofit Statement of Activities Knowledge Check

Test your knowledge of the nonprofit Statement of Activities by taking the quiz below.

Additional Nonprofit Financial Reporting Resources

The nonprofit Statement of Activities is required by GAAP, but it’s also a useful document for assessing financial performance. By contextualizing the data in this document, you can better understand how your organization uses its resources and how it can improve its allocation decisions going forward.

Compiling and analyzing this statement can be a complex process. If you need assistance, our nonprofit financial management experts at YPTC can help you prepare and evaluate your financial statements. Contact us today to get started.

To learn more about nonprofit financial statements, check out the following resources:

- Demystifying the 4 Main Nonprofit Financial Statements. Receive a comprehensive overview of the main nonprofit financial statements and their importance.

- What Is a Nonprofit Balance Sheet? Breaking Down This Report. Learn more about how to prepare and interpret your nonprofit Statement of Financial Position.

- Nonprofit Cash Flow Statement: FAQs and How to Interpret It. Dive deeper into the nonprofit Statement of Cash Flows and what it can tell you about your organization.

Jennifer Alleva

Jennifer Alleva is the Chief Executive Officer at Your Part-Time Controller, LLC (YPTC), a leading provider of nonprofit accounting and financial management services, a Top 100 Firm, and #1 on Accounting Today’s list of Best Firms to Work For. Jennifer brings over three decades of expertise in accounting and leadership to her role as CEO of YPTC.

When Jennifer joined YPTC in 2003, the firm consisted of just over 10 staff members. Since then, she has helped develop YPTC into one of the fastest-growing accounting firms in the country.

Jennifer’s accomplishments include her tenure as an adjunct professor at the University of Pennsylvania Fels Institute, her frequent speaking engagements on nonprofit financial management issues, and her role as the founder of the Women in Nonprofit Leadership Conference in Philadelphia. In addition, from 2021-2024, she hosted the Mission Business Podcast, which spotlighted professionals and narratives from the nonprofit sector.