Nonprofit Board Governance: A Practical Framework

Updated On: 07/07/2026

Posted On: June 4, 2026

Strong nonprofit governance starts with three things: clear roles, reliable financial information, and a consistent review cadence. When those pieces are in place, boards can spot risk sooner, ask better questions, and stay focused on mission.

Governing boards have a fiduciary responsibility, which is a legal and ethical obligation to act in the best interest of the organization they serve. This responsibility is divided into three core duties:

- Duty of care (be informed and engaged)

- Duty of loyalty (act in the organization’s best interest and manage conflicts)

- Duty of obedience (follow laws, mission, and governing documents)

Financial governance is one of the most tangible ways boards fulfill their fiduciary duties. But they need the right financial information, at the right level, at the right time to spot risk, ask better questions, and make decisions that protect the mission. When accounting operations and governance practices are aligned, nonprofits are better equipped to protect resources and fund the mission, strengthen internal controls, and approach audits with confidence.

This guide includes a practical framework you can adapt to strengthen your nonprofit’s financial governance, including:

- Clear roles for the board, finance committee, treasurer, audit committee (if applicable), and management

- Review cadence recommendations—monthly, quarterly, and annual—including what each group should review and discuss

- Tools to improve oversight: board-ready reporting, key questions to ask, common red flags, and critical yearly touchpoints

Financial Governance Roles: Who Does What?

Unclear boundaries between board governance and management can weaken financial governance. Financial oversight works best when everyone understands their lane—especially in smaller nonprofits where a “working board” may be more hands-on. The goal is for board members to oversee and ask informed questions, while management executes and the accounting function produces reliable, timely information.

The Board: Fiduciary Oversight

A nonprofit board’s financial role is strategic and fiduciary. Board members are typically responsible for:

- Approving the annual budget

- Reviewing financial performance and trends

- Ensuring appropriate internal controls, risk management, and core financial policies

- Overseeing executive leadership and compensation, including hiring, supporting, and evaluating executives

- Safeguarding long-term financial health through reserves planning, oversight of the audit, and review of the Form 990 before filing

For large, mature organizations, board members should not be booking journal entries or reconciling bank accounts. Instead, they should focus on asking informed questions, understanding financial implications, and ensuring accountability.

Effective boards rely on financial reports that clearly explain:

- Where the organization stands financially

- How results compare to budget and expectations

- What risks or decisions require board attention

The Treasurer: A Connector

In many nonprofits, the board treasurer helps translate financial information for other board members and supports a strong finance committee. The treasurer role varies by organization maturity—but it works best when it is oversight-oriented (review, questions, and follow-through), rather than stepping into accounting tasks. The treasurer role typically includes:

- Partnering with management to ensure the board receives clear, timely financial reporting

- Helping set expectations for the monthly close and review process

- Leading or supporting the finance committee and escalating key issues to the full board

- Supporting audit and Form 990 review processes alongside the audit committee

When helpful, an outsourced controller or CFO partner can support treasurers’ board and committee conversations by providing board-ready reporting and joining meetings to walk through financial results and risk areas.

The Finance Committee: The Board’s Finance Arm

The finance committee acts as the board’s financial extension. It typically:

- Reviews financial matters and documents prior to full-board review (e.g., budget, audit report, and Form 990)

- Reviews detailed financial statements and variances

- Oversees internal controls and policies

- Monitors cash flow, reserves, and financial risk

- Serves as a sounding board for management and accounting partners

A strong finance committee focuses on interpretation, controls, and forward-looking questions—and helps ensure the board receives the most important financial signals without getting lost in the numbers.

When nonprofits outsource controller or accounting functions, the finance committee often becomes a critical partner in reviewing work products, discussing trends, and reinforcing governance discipline.

The Audit Committee: Independence and Accountability

Some nonprofits establish a separate audit committee; others handle audit oversight within the finance committee. Either way, nonprofits should ensure an independent review of financial statements and internal controls and create a clear channel for the external auditors to communicate with the board.

The audit committee typically takes on the following tasks:

- Recommend the selection of the audit firm (or review/compilation provider, as applicable)

- Review the audit plan, timeline, and key risk areas

- Meet with auditors to review results, findings, and management letter recommendations

- Track remediation of internal control gaps and process improvements

Finance Management: Execution, Accuracy, and Financial Clarity

A nonprofit finance department’s management team may include a CFO, finance director, controller, and finance or accounting managers. Whether in-house or outsourced, this team is responsible for:

- Managing day-to-day financial operations

- Executing the budget and financial plan

- Ensuring transactions are accurate, timely, and compliant

- Implementing internal controls

- Communicating financial results and risks to executive leadership and the board

This level is where accounting quality matters most. Without reliable month-end-close processes, reconciliations, and reporting, the board cannot govern effectively.

YPTC’s accounting and controller services are provided by experienced professionals who understand nonprofit organizations. We ensure accuracy and reliability in your financial information by taking ownership of:

- Month-end close and reconciliations

- Financial statement preparation

- Budgeting and forecasting

- Internal reporting and dashboards

- Audit preparation

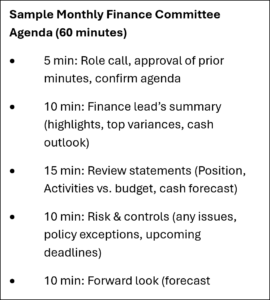

Governance in Practice: A Realistic Review Cadence

In addition to clear roles, strong governance also depends on regular financial reviews.

Monthly: Close, Clarity, and Early Warning Signals

At a minimum, nonprofits should review core financial reports monthly. Finance management reviews more frequently, but the finance committee typically does the deeper monthly dive and elevates key items to the full board at regular board meetings. Monthly reviews help leadership and finance committees:

- Identify budget variances early

- Monitor liquidity and cash flow

- Spot internal control issues before they escalate

- Make informed, real-time decisions

The finance committee’s monthly review should include:

- Statement of Financial Position

- Statement of Activities (actuals vs. budget)

- Cash flow updates or forecasts

- Key operational or financial metrics, as relevant

Monthly questions to ask (board/finance committee):

- Do we understand the top 3 variances (favorable or unfavorable) and whether they are due to timing vs. true performance?

- Is cash projected to be adequate over the next 60–90 days? What assumptions does the forecast rely on?

- Are we honoring donor restrictions and grant requirements, including spending timelines?

- Are there any new contracts, staffing changes, or program expansions that materially change our financial outlook?

- Are there any control issues or process breakdowns we should address now (e.g., late reconciliations, missing approvals)?

Common monthly red flags include:

- Unexplained or recurring variances

- Consistently late monthly closes

- Large unreconciled balances

- Aging receivables (60-90+ days)

- Frequent one-time adjustments

- Unanticipated cash shortages

A disciplined month-end close process is essential. Consistent and timely reconciliations and reviews produce accurate, decision-ready reports and keep your nonprofit audit-ready year-round.

Quarterly: Trend Analysis, Forecasting, and Strategic Adjustment

Quarterly reviews allow boards and finance committees to step back from month-to-month details and look for patterns. This is often where governance moves from fiduciary oversight into more strategic discussions about what’s changing in the environment that should reshape assumptions and operational choices.

Board members might ask questions such as:

- Are revenue assumptions holding?

- Are expenses tracking as expected?

- Are reserves or cash balances changing?

- Do forecasts suggest a need to adjust strategy?

Quarterly is often the right interval for:

- An updated forecast for the remainder of the year (and next year, if feasible)

- Scenario planning (best case/expected/worst case) with agreed-upon triggers for specified actions

- A closer look at program economics, major grants and contracts, staffing plans, or reserve targets

Quarterly forecasting and scenario planning can be especially valuable for nonprofits navigating grant timing, seasonal revenue, or program expansion issues because it creates space for proactive management.

Annually: Budget, Audit, Form 990, and Policy Updates

Annual financial governance milestones typically include:

- Budget development and approval

- Year-end financial statements

- Audit or financial review coordination

- Form 990 review

- Policy and internal control review

While all these steps are critical, the last three are worth emphasizing because they tend to be ones that many nonprofits skip:

- Ensure the board (or audit committee) has an opportunity to meet with the auditors about results and recommendations.

- Have the full board review the Form 990 before it is filed. The 990 is a public document and often the first place funders and stakeholders look for governance and financial transparency.

- Policies to revisit (confirm or update) annually include conflicts of interest, whistleblower, document retention, expense reimbursement, and delegated authority/approval thresholds.

Governance Works Best When the Numbers Work

Effective nonprofit governance requires:

- Clear roles

- Reliable information

- Consistent review cadences

- Accounting systems built to support oversight

When financial governance and accounting execution are aligned, boards receive relevant, reliable, and easily digestible financial information and can carry out their oversight duties more efficiently and effectively.

How YPTC Supports Financial Governance in Practice

YPTC’s services are designed to reinforce financial governance by helping nonprofits establish reliable reporting, streamline processes, and make oversight easier and more consistent. Support may include:

- A consistent month-end close and board-ready financial statements

- Finance committee support: narratives, dashboards, and meeting prep so discussions stay decision-focused

- Attendance at board/committee meetings to explain results, answer questions, and flag emerging risks

- Budgeting, forecasting, and scenario planning tied to strategic priorities

- Internal control design, documentation, and remediation planning

- Audit preparation, including schedules and workpapers and board/audit committee communication

- Training and education for board members without finance or accounting expertise

YPTC helps nonprofits anticipate and respond effectively to board needs, resulting in more

confident, informed, and proactive governance.